The International Energy Agency has just released its annual Medium-Term Coal Market Report (MCMR) and reports that “coal’s share of the global energy mix continues to rise, and by 2017 coal will come close to surpassing oil as the world’s top energy source”.

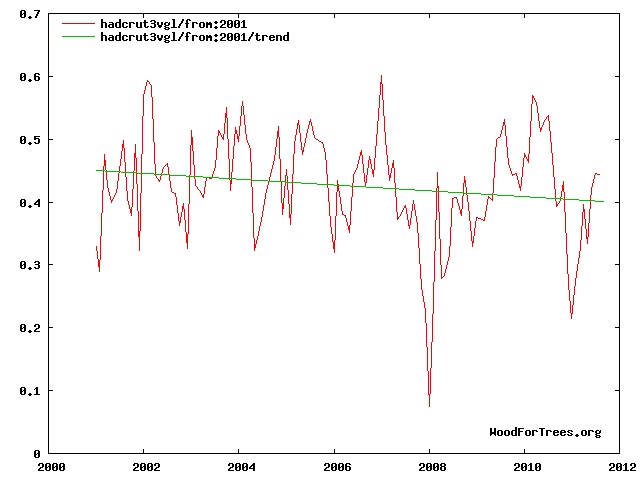

Yet global temperatures have not risen for 16 years and continue to decline. And the demonisation of the use of coal has increased electricity prices quite unnecessarily. The end of the world will not happen either on 21st December 2012 or by the use of fossil fuels.

In a press release the IEA says:

“Thanks to abundant supplies and insatiable demand for power from emerging markets, coal met nearly half of the rise in global energy demand during the first decade of the 21st Century,” said IEA Executive Director Maria van der Hoeven. “This report sees that trend continuing. In fact, the world will burn around 1.2 billion more tonnes of coal per year by 2017 compared to today – equivalent to the current coal consumption of Russia and the United States combined. Coal’s share of the global energy mix continues to grow each year, and if no changes are made to current policies, coal will catch oil within a decade.”

China and India lead the growth in coal consumption over the next five years. The report says China will surpass the rest of the world in coal demand during the outlook period, while India will become the largest seaborne coal importer and second-largest consumer, surpassing the United States.

The report notes that in the absence of a high carbon price, only fierce competition from low-priced gas can effectively reduce coal demand. “The US experience suggests that a more efficient gas market, marked by flexible pricing and fueled by indigenous unconventional resources that are produced sustainably, can reduce coal use, CO2 emissions and consumers’ electricity bills, without harming energy security,” said Ms. van der Hoeven. “Europe, China and other regions should take note.”

While coal consumption and carbon dioxide have been rising, global temperatures have not been paying any attention – much to the dismay of alarmist models.

Global temperature decline

IPCC alarmist models versus reality

Model predictions versus observations

The IEA factsheet goes on:

- Coal demand is growing everywhere but the United States. The trend of the last decade continued in 2011, with coal supplying near half of the incremental primary energy supply globally. Coal demand grew 4.3% in 2011, or 304 million tonnes (mt). Chinese demand grew by 233 mt. The only region where coal demand declined was the United States. That drop is neither policy-driven nor a consequence of recession but rather the result of the availability of cheap gas.

- Even though coal demand growth is slowing, coal’s share of the global energy mix is still rising, and by 2017 coal will come close to surpassing oil as the world’s top energy source. The world will burn around 1.2 billion more tonnes of coal per year by 2017 compared with today. That’s more than the current annual coal consumption of the United States and Russia combined.

- China has become the largest coal importer in the world. In 2009, China became a net coal importer for the first time. In 2011, it became the largest coal importer, surpassing Japan, which had held the position for decades. Chinese imports (including Hong Kong) reached 204 mt in 2011 and they continued to grow in 2012.

- Indonesia has become the largest coal exporter in the world. As another example of the increasing weight of non-OECD countries, Indonesia surpassed long-standing leader Australia as the largest exporter on a tonnage basis. Floods in Queensland in 2010-2011 constrained Australian exports, while Indonesia growth did not stop, surpassing the 300 mt line.

- The coal renaissance in Europe is only temporary. Low CO2 and high gas prices plus coal oversupply coming from US have made coal more competitive than gas for power generation, triggering coal consumption. However, increasing use of renewables, retirement of coal plants, and more balanced gas and coal prices will decrease coal consumption in most of Europe. All in all, coal demand in 2017 will be 10 million tonnes coal equivalent (mtce) higher than in 2011, as growth in Turkey will offset the more general decline.

- Bad times for US coal. The fiercest competition for coal occurs in United States, where gas has gone below the $2/MBtu line. Whereas exports recently could alleviate the plight of US coal producers, declining demand will give rise to cuts and layoffs in mines, especially in the high-cost Appalachia area. Medium-Term Coal Market Report 2012 projections for US coal demand by 2017 are 600 mtce, a dramatic fall from 697 mtce in 2011. US production is projected to fall from 771 mtce in 2011 to 697 mtce in 2017.

- India will increase its influence in coal markets. Endowed with large coal reserves, a population of more than 1 billion, electricity shortages and the largest pocket of energy poverty in the world, India makes the perfect cocktail to boost coal consumption. Domestic industry’s performance will allow India to be the largest seaborne coal importer by 2017 with 204 mtce and the second-largest coal consumer, surpassing United States.

- Australia will recover its throne as the biggest coal exporter. Despite some issues such as rising labour costs and domestic currency rate, which give Indonesia competitive advantages, Australia will concentrate a great share on infrastructure and mine expansion investments to become the largest exporter, with 356 mtce by 2017, well above Indonesia’s total exports then of 309 mtce.

- Enough investments are planned and in progress to ensuresupply. Uncertainties will delay or cancel many of them. In the pipeline are almost 300 million tonnes per annum (mtpa) of terminal capacity and the 150 mtpa (probable) to 600 mtpa (potential) of mine expansion capacity, more than enough to meet coal demand in a secure way over the outlook period. But current low prices and uncertainty about economic growth, especially when related to China, will delay and stop some investments.

MCMR 2012 is for sale at IEA bookshop.

Tags: climate change, IEA, IEA Coal Market Report, International Energy Agency