The mysterious goings-on at the whistle-blower fracas at the Queensland University of Technology seem to run quite deep. The mystery is apparently compounded by commercial interests. The elements include a company spun-off from QUT (Tissue Therapies), University staff owning stock in the company, the company raising start-up money, listed on the stock exchange and having a value entirely dependent upon the prospects for one breakthrough product (VitroGro).

The latest revelation suggests that the whistle- blowers, Luke Cormack and another – whose identity is protected but was “inadvertently” revealed by the University Vice Chancellor – have been spied upon. Cormack was given “counselling” organised by the University – which counselling was never confidential. The contents of these discussions were apparently reported by the counselor to the University authorities!! Seems to be a remarkable absence of ethical standards at the University and – more particularly – with the counselor. Perhaps it was all “inadvertent”.

A summary of the story is here in the Courier-Mail.

His colleagues had discovered a cheaper and more reliable way to grow human tissue, with huge implications for biology and medicine. Cormack’s research concerning stem cells aimed to build on their findings.

But no matter what he tried, his cells refused to grow. He later failed his PhD.

The key question is whether VitroGro has real prospects or is just hype. It is supposed to be used in healing wounds by helping cells to grow. If VitroGro’s potential benefits have knowingly been hyped by the “inadvertently” manipulated data, then there is a risk that this is all a start-up scam.

Business start-up scams depend upon inflating the apparent value of a start-up company by promoting perceptions of a bright future such that investment money can be attracted.

For example, the founders of the start-up put in say 10 and raise say 90 with a few select investors. Hype then increases the apparent value of this 100 to say 1,000 (and there have been cases of reaching even 10,000) – all based on perceptions of prospects. The initial investors cash in through a listing on the stock exchange essentially spreading the risk by drawing in a great number of small shareholders. If there is no substance to the start-up, operations are prolonged as long as possible where the company’s officials know they have a limited time available to extract salaries or consultancy fees before the house of cards collapses. If there is no substance to the start-up, it eventually collapses and a large volume of small shareholders lose whatever they had put in. The initial investors have long since exited though they may keep a small stake until the bitter end just to delay the inevitable end, prolong the period available for extraction of all that can be extracted and for public relations.

Start-up risk is always high of course and most start-ups are genuine and not scams – but they do have a very high death rate. Trying to separate the scams from the genuine cases is not so easy.

But “inadvertent” falsification stretches credulity and raises a warning flag.

In December 2012, Retraction Watch commented:

What also caught our notice is that senior author Zee Upton is consulting chief scientific officer of Tissue Therapies, which QUT spun off to develop technologies based on vitronectin and other compounds. She and other investors co-founded the company in 2003, approached QUT for a license on the intellectual property, and had Tissue Therapies listed on the Australian Stock Exchange in 2004, according to an Upton presentation available on the QUT website. An eprint of another paper by Upton and co-authors available on the QUT site notes that several authors had bought stock in the company:

The Authors have purchased shares in Tissue Therapies Ltd., an enterprise spun-out from the Queensland University of Technology, Brisbane, to commercialize some of the technology described in this manuscript.

That all seems to us like a conflict of interest for both the authors and for the university investigating the research. None of that was disclosed in the now-retracted paper, however.

In February this year we learnt that:

TISSUE THERAPIES

Tissue Therapies has raised $8.7 million in a placement and hopes to raise a further $4.5 million through a one-for-10 non-renounceable rights issue at 21 cents a share. Tissue Therapies said the record date for the rights issue was March 7, with the offer opening on March 12 and closing on March 26, 2013. The company said the funds would be used to further advance commercialization of the Vitrogro wound treatment. Tissue Therapies said that Bell Potter and RBS Morgans were joint lead managers for the capital raising and rights issue.

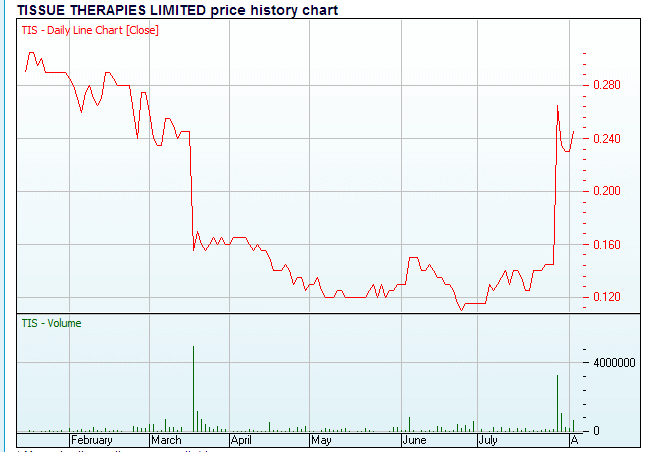

This year the Tissue Therapies share price looks like this and of course the volume offloaded may be as important as the price:

Tissue Therapies Share price 2013

It appears that VitroGro is being classed as a “device” in Europe:

- After market close in Australia on Friday 26 July 2013, the MHRA confirmed by letter to both Tissue Therapies and BSI that VitroGro® ECM is classified as a device. The Company has forwarded the MHRA classification confirmation letter to the EMA.

- The MHRA confirmed the final classification of VitroGro® ECM as a device during late October 2012. (Please see ASX: TIS “VitroGro® ECM Medical Device Classification Confirmed”, 30 October 2012.)

- While a firm timetable for the data review by the EMA and granting of CE Mark has not yet been established, a clear process to achieve CE Mark has now been provided by the MHRA and EMA.The EMA review of manufacturing quality data is the last step in the process of granting CE Mark and the start of sales. This data review is a desk audit for which Tissue Therapies is well prepared.

And not so very much should have been “inadvertent”.

Tags: Courier-Mail, Luke Cormack, Queensland University of Technology, QUT, retraction, Tissue Therapies, VitroGro, whistle blower