Archive for the ‘Economy’ Category

March 26, 2013

The wunderkind of the EU have just established a two-currency Europe and have undermined the trust any depositor can have in a Eurozone bank. The Cyprus solution has effectively created a Cypriot Euro which is – in practice – worth a lot less than a normal Euro. And every depositor holding more than €100,000 will be taking a very large risk if he puts his money in a weak Eurozone bank or in a weak Eurozone country. The depositor will need to demand a risk premium to cover the risk that his money could be stolen by the bank or by the State.

A Cypriot Euro (Κ€) is now worth less than a “normal” Euro (€). What that value is is a little difficult to judge but it lies somewhere between 60% and 90% of a normal Euro. All K€ which are outside of the deposit guarantee are now only worth 80% of a normal €. Moreover currency restrictions apply which are not so different to exchange control regulations for movement outside the country but which apply – in addition – to movement of money within Cyprus. A K€ still has the same buying power as a normal Euro but, on the other hand, it will no longer be possible to get any “outside Euros” to move into Cyprus and risk confiscation!

Jeroen Dijsselbloem, the Dutch chairman of the Eurozone announced (rather idiotically) yesterday that the Cyprus solution was the template to be used in the future. Cyprus itself does not have an economy large enought to be so significant. But effectively he was confirming that “Savings accounts in Spain, Italy and other European countries will be raided if needed to preserve Europe’s single currency by propping up failing banks”. But the resulting, ostensibly “single currency” will , de facto, have to distinguish between the currency held in different countries and just calling it a “single” currency will not hide the reality. Mr. Dijsselbloem later tried to back-pedal on his statement but the truth was out by then. No amount of denials will change the fact that the Cyprus solution now sets the precedent and every weak bank will now be required to try and protect its shareholders by attacking its depositors.

I think the damage has been done and it is already too late for the EU to try and soften the message. I heard today that financial advisers in India and China were already suggesting to clients with Euro holdings to make sure it was in a strong country. This eliminates Greece, Italy, Spain, Ireland and even Hollande’s France. This only leaves Germany. The Russians are probably already shifting their legitimate Euro funds to Germany or the Netherlands and their not-so-legitimate money to the Bahamas or Mauritius or the Seychelles. In the short term Germany is the main beneficiary. Not only are their exports being helped by a weak Euro (kept weak because of the weak countries persisting within the Euro) but their banks are likely to see Euro deposits from the weak countries moving their way. But in the long term a flight from the Euro will not help anyone in Europe. The ideological – and almost dogmatic – attachment to the single Euro is now damaging all of Europe and delaying the recovery. Every single one of the bailed-out countries would recover faster if only they had a currency which could have been devalued.

The Cyprus solution is also a more general attack on Europe’s middle class (admittedly the richer part of the middle class). The population of the EU is about 500 million. With an average of about 2.5 individuals per household this represents about 200 million households. Probably 15-20 million households have a net worth exceeding €200,000 which implies financial assets (as opposed to property and other non-liquid assets) of about €100,000. So an attack on European deposits of greater than €100,000 could affect some 40 – 50 million individuals.

Cyprus could be the straw that breaks the Euro’s back.

Tags:Cyprus, Euro, European Union, Eurozone, Jeroen Dijsselbloem, Two currency Europe

Posted in Behaviour, Currency, Economy, European Union, Politics | Comments Off on Cyprus could be the straw that breaks the Euro’s back

March 23, 2013

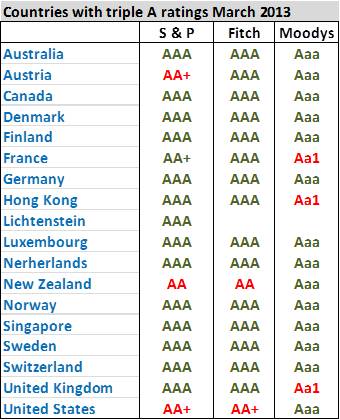

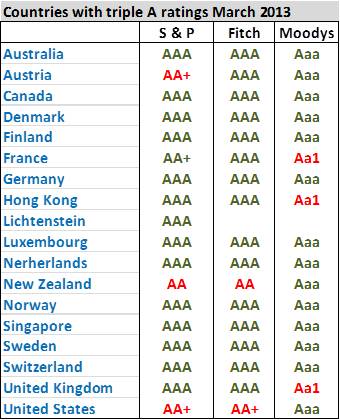

As Fitch puts the Uk’s country rating on negative watch, the number of countries left with triple A ratings has continued to shrink in 2013. Only countries given a triple-A rating by at least one of the big-3 rating agencies are included here.

Tags:Credit rating, Fitch, Moody, S & P

Posted in Economy, Politics | 1 Comment »

January 10, 2013

China’s role as a motor for the world economy continues.

In spite of sluggish world-wide demand, Chinese exports rose 7.9 percent in 2012 from the previous year, while imports climbed 4.3 percent year on year. Xinhua reports that “China’s foreign trade for 2013 will be better than that of last year despite uncertainties, a General Administration of Customs spokesman said on Thursday. Spokesman Zheng Yuesheng said global economies have launched stimulus policies to prevent growth rates from slumping, adding that China’s domestic efforts to boost the growth of foreign trade will have more visible effects this year”.

MarketWatch: China’s trade surplus soared to $31.6 billion in December, trouncing estimates and widening sharply from a $19.6 billion surplus in November, aided by a strong growth in the country’s exports. Official data released Thursday showed exports expanded 14.1% during the month from the year-earlier period, while imports grew 6%. A survey of economists by Dow Jones Newswires estimated a trade surplus of $19.6 billion, exports growth of 4.6% and a 3.3% increase in imports. The steep increase in December’s positive trade balance boosted China’s full-year trade surplus for 2012 to $231.1 billion, 48.1% higher than the level recorded in 2011, according to a Xinhua news report.

Tags:balance of trade, China, Economy, Export, International trade

Posted in Business, China, Economy | Comments Off on China’s trade surplus in 2012 was 48% higher than in 2011

January 2, 2013

Well, Obama got some tax increases for the wealthy and a postponement of the fight for spending cuts. The fiscal cliff was little more than a fiscal bump. Republicans are more upset than Democrats – at least judging by the “squeal index” – and the Democrats actually prevailed over the Republican majority in the House of Representatives. So, the view from across the Atlantic based on the belief that the loser squeals the loudest, is that Obama must have won. (The splits in the Republican Party are particularly interesting since these may completely nullify their majority in the Congress!)

But whatever it was that was agreed to, the US debt will rise by some $4 trillion directly as a consequence of this “deal”. The US follows exactly the same way as Europe in putting off the day when the music must be faced. The fight about spending and debt will come in about two months. Years of profligacy and living beyond available means cannot just be wished away. Just wishing that the economy will rebound – faster than has ever happened before – and will increase revenues so that spending cuts can be avoided is not living in the “land of hope” but is living in a fantasy. It is the same fantasy being played out in Europe. Obama is merely following Francois Hollande’s super-tax on the very rich to postpone the cuts in spending that are desperately needed and must come. The fundamental rule of party politics is being upheld: “Tax the voters for the other party and spend on your own”. The pain to come is inevitable. Of course, those who have been profligate have taken their benefits and gone. The pain will have to be borne by others – in the US as in Greece and Spain and Italy. I can’t help suspecting that the goal – whether for Hollande or for Obama – is to just postpone the evil day of spending cuts long enough so that it happens on someone else’s watch. But both Obama and Hollande are at the start of new terms and neither will be able to avoid facing reality.

The high drama at the end of the year in the US bears a strong resemblance to a Christmas farce. It couldn’t possibly have been a pantomime since any kind of music was notably absent. Obama’s performance on the 31st of December was badly out-of-tune and a little embarrassing to watch. And the other bit-players on display – Biden and Reid and Boehner and Cantor and McConnell – with their self-adulation, self-congratulations and mutual admiration were even worse.

Tags:Barack Obama, Democrats, Fiscal Cliff, Republicans, United States public debt

Posted in Economy, Europe, Politics, US | Comments Off on Obama – sort-of – wins the “fiscal cliff” and goes the way of Europe

December 26, 2012

No doubt I have a simplistic view but the best thing in the long-term for the world economy would be for the US to start reducing its budget deficit and its burgeoning public debt. Public debt has to be set to whatever level is sustainable. An economy in transition from one level to another can permit a changing level of public debt, but the current level of deficits (7 -9% of GDP) and ever-increasing debt is not sustainable. The problem is that even if the US did not avoid the fiscal cliff the US public debt would continue to grow – if a little more slowly than as at present. The cliff may in reality be more like a hill but it is still along the way to the wrong place.

US Public Debt

Budget discipline and a stable level of public debt must – I think – come first. It is public profligacy – whether in Greece or Spain or the US – which is unsustainable and rampant profligacy will not end without some short-term pain. It is probably time for the US to bite the bullet.

I see that the US press is now beginning to expect that some kind of fall – whether over a cliff or a hill – is inevitable but that perhaps the fall can be cushioned by attaching a bungee rope or by aiming for a ledge part-way down!

NY Times: Until late last week, most observers had expected the president and Congressional Republicans to come up with at least a short-term compromise before the year-end deadline. But thefailure of Speaker John A. Boehner to win support for tax increases on the wealthiest Americans from fellow House Republicans has forced many economic observers to reconsider what might happen if political leaders remain deadlocked into 2013.

MSNBC: On the Sunday news shows, no one signaled a change of position that could form the basis for a short-term fix, despite a suggestion from Obama on Friday that he would favor one. The focus was shifting instead to the days following January 1 when the lowered tax rates dating back to the George W. Bush administration will have expired, presenting Congress with a redefined and more welcome task that involves only cutting taxes, not raising them.

“I believe we are,” going over the cliff, said Republican Senator John Barrasso of Wyoming. “I think the president is eager to go over the cliff for political purposes. I think he sees a political victory at the bottom of the cliff,” Barrasso said on Fox News Sunday.

Some Republicans have said Obama would welcome the fiscal cliff’s tax increases and defense cuts, as well as the chance to blame Republicans for rejecting deal. Obama has rejected that assertion.

WSJ: Lawmakers returning to town this week will see whether they can agree on a plan to avoid the full brunt of the fiscal cliff, the combined $500 billion in tax increases and spending cuts set to begin next week. Little if any progress was made in the talks before Congress and President Barack Obama left town last Friday for Christmas. The president plans to leave his vacation in Hawaii late Wednesday night, returning to Washington on Thursday, the White House said.

CNBC: Despite the $600 billion of tax hikes and spending cuts due to come into force at the end of this month unless U.S. lawmakers reach a deal, the S&P 500 index is not displaying signs of stress, says independent chartist Daryl Guppy.

The stock index is in fact trading upwards as investors increasingly take in the possibility that the U.S. economy might fall over the “fiscal cliff,” he told CNBC Asia’s “Squawk Box” on Thursday. “The fiscal cliff is a bungee jump. It used to be exciting. Now it’s just a tourist attraction. The market is absorbing that,” he said.

While the S&P 500 index has dipped back towards the 1,380 to 1,400 range seen in August and mostly recently in November, stocks appear to be on their way up again, he added. The index closed at about 1,419 on Wednesday.

Tags:Economy, Fiscal Cliff, Public spending, Taxes, US Public Debt

Posted in Business, Economics, Economy, Politics, US | Comments Off on US going over the fiscal cliff is probably best for world economy

November 23, 2012

It should have been and should be patently obvious that subsidy regimes are largely counter productive, but such is the power of self-righteous, environmental correctness – which is the modern face of fascism – that many more jobs will be lost and much more tax-payer’s money squandered before sanity will prevail again. Further job losses in the UK were announced by Tata Steel just as the government announced plans to triple the burden on consumers for further nonsense subsidies for “green” power.

(more…)

Tags:Department of Energy and Climate Change, environmental fascism, green subsidies and job losses, Tata Steel, vlimate change

Posted in Alarmism, Climate, Economy, Energy | Comments Off on “Green” subsidies increase energy prices which leads to fewer jobs

September 18, 2012

The latest Mitt Romney “gaffe” is getting much attention. But I was a little surprised to find that while what he said may well be a gaffe in electoral terms – and he may even have lost the Presidential election here – his statement was actually quite correct. I had not appreciated that almost half of all US households paid no federal income tax at all. In the US, federal income tax is a major source of tax revenues and contributes about half of all tax revenues (tax revenues about 15.4% of gdp in 2011 with federal income tax providing 7.3% of gdp). Romney in his leaked video said:

(more…)

Tags:Income tax, Mitt Romney, Tax, Taxation, United States, wealth creation

Posted in Behaviour, Economy, Politics, US | Comments Off on Tax on income is easy to levy but fundamentally unsound

May 6, 2012

Sarkozy has lost in France according to Belgian and Swiss sources though the exit polls in France are not yet out. Hollande is expected to win by 5%.

The exit polls are also out in Greece.

In Greece, the only two parties supporting the Eurozone bailout and the austerity measures – PASOK and New Democracy – will probably not be able to form the next government. And that means that the chances of Europe leaving the Euro are greatly enhanced. In the short term this will cause massive turbulence in the Eurozone.

(more…)

Tags:Elections, Euro, Eurozone, France, Greece, New Democracy, Nicolas Sarkozy, PASOK

Posted in Economy, European Union, France, Greece, Politics | Comments Off on More turmoil awaits Europe as Sarkozy loses and Greeks vote against Europe

November 14, 2011

I have faith in Japanese resilience and will still stick my neck out and stay with my forecast that the Japanese economy will become a global “driver” through 2012 and 2013.

Japanese Gross Domestic Product grew by 1.5 % over the 3rd quarter (July – September) representing an annualized growth rate of 6 percent. This is the fastest rate of growth for 18 months. The Cabinet Office said today in Tokyo that at 543 trillion yen ($7 trillion), the economic output was back to levels last seen before the March 11th Great Tohoku quake and tsunami.

The growth seems to have been led by exports rather than the domestic impetus measures to recover from the earthquake or the subsequent spending on rebuilding infrastructure. These probably need 2 more quarters to kick-in but that means that this growth is still vulnerable to current global weaknesses.

However the optimistic “glass half full” view would be that Japanese exports have grown mainly to Asia and the earthquake rebound has yet to come. Moreover this has happened in spite of a very high Yen. Any recovery in Europe and N. America would be a further boost to an economy which is large enough to then act as a global motor.

NY Times:

The rebound underscores the speed at which Japanese industry has been able to get back on its feet after the March 11 earthquake and tsunami, rebuilding factories and re-establishing supply chains severed by the destruction.

Exports jumped 6.2 percent as manufacturers got production back on track. Private consumption, which accounts for almost two-thirds of Japan’s economy, grew 1 percent, helped by a rebound in consumer sentiment and replacement demand in the tsunami zone.

Still, policy makers and economists also worry that the punishingly strong yen of recent months as well as weak growth in major trading partners, like the United States and China, will take a toll on Japanese exports. The crisis at the Fukushima Daiichi nuclear plant, meanwhile, has thrown the country’s energy policy into disarray and cast a pall over Japan’s recovery.

Related: Could the disaster in Japan power a wave of sustainable growth?

Tags:Economy of Japan, GDP growth, Great Tohoku quake and tsunami, Gross domestic product, Japan

Posted in Economy, Japan, Natural Disasters | Comments Off on Japan back to growth with a bang with GDP up 1.5% in 3 months

November 7, 2011

Image via Wikipedia

Il Cavaliere , Sylvio “bunga-bunga” Berlusconi is 75 years old, has a personal fortune of some $9billion, and has been Italy’s Prime Minister for longer than anyone else. He is clinging desperately to power as Italy slides towards a Greece-like crevice and it is not apparent as to why he bothers. Whereas the Greek debt is only about 4% of Eurozone debt, Italy’s debt is closer to 20%. Italy’s public debt in 2010 was 118.4% of GDP. The annual budget deficit was 4.6% of GDP. Italy’s public debt-to-GDP ratio is the second highest in the euro zone after Greece’s, while its debt in absolute terms, which stood at 1.84 trillion euros at the end of 2010, is second to Germany’s.

It might seem to be just a powerful politician in denial of the approaching flames when Berlusconi declares that “Life in Italy is good. The restaurants are full. It’s difficult to get a seat on a plane they’re so busy; holidays are all booked up”.

(more…)

Tags:Bunga bunga Berlusconi, European Union, Eurozone, Greece, International Monetary Fund, Italy, Silvio Berlusconi

Posted in Economy, Ethics, European Union, Italy, Politics | Comments Off on Berlusconi bungas while Italy burns