All electric cars shift emissions from the exhaust pipe of the vehicle to the place where the electricity is generated. The actual mix of fuel sources used to feed the grid then represent the emissions profile of electric cars. The efficiency of electric cars from generation of electricity to wheel-power is not much different from gasoline based automobiles and clearly inferior to diesel engines.

Fossil fuels used directly in vehicle internal combustion engines have a thermal efficiency ranging from 37% for gasoline to over 55% for very large marine diesels.

source JSME

For electricity generation the thermal efficiency varies from less than 30% to over 60% for coal, oil, gas, solar thermal or nuclear power plants. Thermal efficiency is meaningless (and undefined) for hydropower, wind power or photovoltaic solar.

An electric car being charged from the grid does so after a further 10% of transmission and distribution losses but only accrues a further 2 – 5% losses through the motor(s) to shaft rotation. (There are further mechanical losses in getting to the rotation of the wheels but these are common to all kinds of motive power).

The emissions due to the use of an electric car are entirely dependant upon the emissions involved in the generation of the charging electricity. If the grid is largely dependant upon coal (India), or coal and gas (US) then the gaseous emissions are higher than for diesel engines but slightly better than for gasoline automobiles. If, the grid is primarily hydropower as in Norway, or primarily hydro and nuclear (as in Sweden) then there are virtually no emissions from electric vehicles.

The fundamental reality is that electric cars are not yet commercially viable (range, weight, charging time and cost). Two decades of subsidies also confirms for me my contention, that subsidies are usually counter-productive, always delay commercialisation and nearly always lead to a focus on milking subsidies rather than commercialising a technology.

A recent Forbes article addresses the fantasies surrounding emissions, and Tesla cars. I wouldn’t mind owning a Tesla car where my acquisition price is heavily subsidised. But now that the initial investors have milked the subsidies, and operations – in spite of the subsidies – have yet to show a profit, I would not invest in Tesla shares.

Earlier this summer, SolarCity, Elon Musk’s rooftop solar company, appeared to be headed toward bankruptcy. So it shocked investors everywhere when Musk’s other brainchild, Tesla Motors TSLA -2.21%, itself struggling, announced plans to acquire the struggling panel maker and installer.

“Tesla Talks Big, Falls Short,” read a headline last week on the front page of the Wall Street Journal. The subtitle: “Car maker has failed to meet more than 20 of CEO Elon Musk’s projections in the past five years.”

Surely combining two wrong businesses won’t make a right one. True, they’re both politically correct. But they’re economically incorrect.

Tesla’s operating losses, along with its fishy accounting practices and unrealistic investor promises, have led Devonshire Research Group to liken the car company’s business model to Enron’s.

Bad entrepreneurship is normally punished by market losses and contraction. But Musk’s market is rigged. A mountain of taxpayer subsidies is allowing Tesla’s bad show to go on — and even expand.Musk’s various ventures have received almost $5 billion worth of government assistance. Nevada recently chimed in with $1.3 billion to incentivize Tesla to build its “gigafactory” — a new battery producing facility — near Reno. Each car sold by Tesla receives a federal income tax credit of $7,500. And California allows an additional $2,500 rebate to its citizens.

Even the White House is throwing cash Musk’s way. President Obama just announced $4.5 billion in loan guarantees for electric vehicle entrepreneurs. According to the president, the money will help fill garages with EVs and make charging stations ubiquitous.

Tesla is redefining “too big to fail” as “politically correct, so bail.”

…..

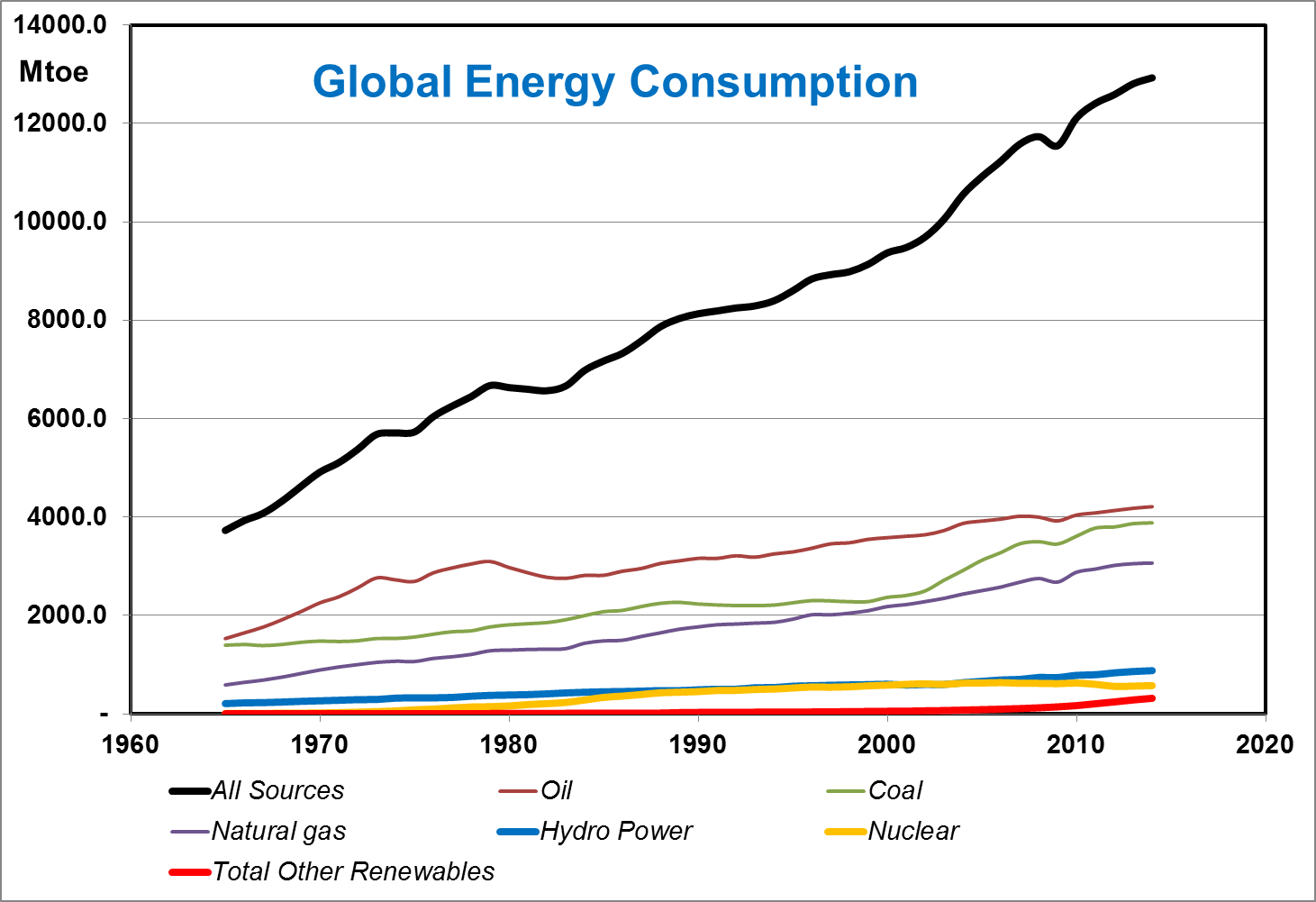

So-called zero-emission vehicles reflect the fuel-profile of electricity generation. 2015 U.S. electricity generation consisted of 33% coal; 33% natural gas; 20% nuclear; 13% renewables; and 1% oil.

Fossil fuels, in other words, have a two-thirds market share for EVs, wind and solar just 5%. Nuclear power, hydropower, and biomass, account for the remainder. …..

…..