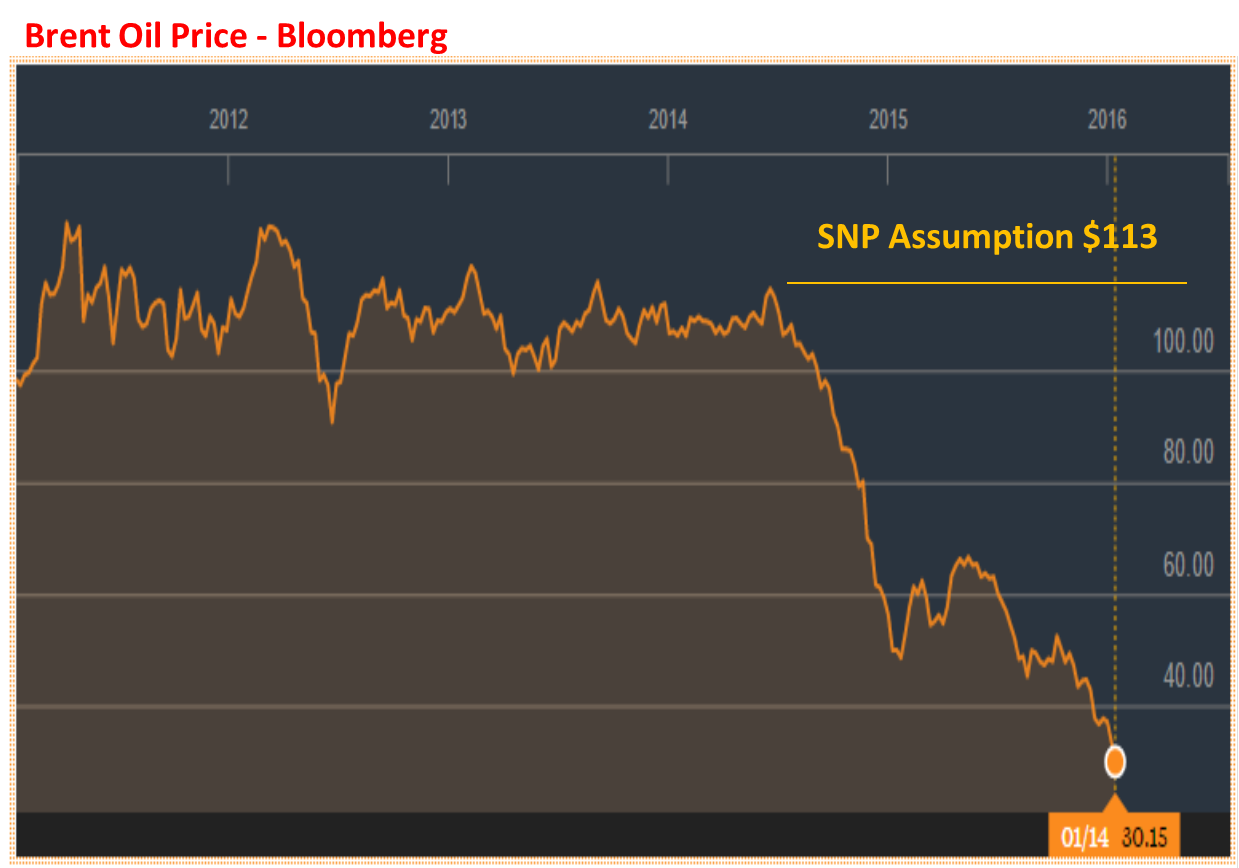

High oil prices at around $100/barrel fueled the first shale oil boom in the US. Drilling rigs proliferated and the ensuing oil glut led to the sharp drop of price in 2015. Saudi Arabia then started a price war for a variety of reasons:

- to attack the shale oil industry (and take away the market share they had won),

- to hurt Iran whose return to the international oil market was imminent, and

- to hurt Russia because of the vulnerability of their budget to oil revenues

But most importantly they wished to attack the shale oil industry which was thought to have its Achilles heel in its relatively high production cost. With Saudi Arabian production cost at around $3/barrel, even a long period at low oil prices was considered a critical advantage. The strategy backfired and Saudi was forced to participate in OPEC’s production cuts to prop up the oil price. But even that action is now backfiring as the shale oil industry has emerged leaner and meaner and is now ramping up production again. Last week the oil price dropped some 10% as shale oil now retakes some of the market share it had lost.

The glut continues and we are unlikely to see prices much above $50-60/barrel for the next 2 or 3 years. The Saudi attacks have only helped shale oil to reduce its own costs dramatically. They are far less vulnerable to attack now than in 2015. At that time they needed an oil price of around $80 to make any reasonable profit. Now they are so much leaner that they are viable at oil prices even as low as $40/barrel (and some wells are now rivaling the Saudi production costs).

Oil Wars

Has OPEC Underestimated U.S. Shale Once Again?

The U.S. shale cowboys are back on their horses and leading a strong recovery in the oil patch that is not expected to falter even as WTI prices dropped last week below $50 per barrel for the first time in more than two months.

With lessons learned from the oil price crash and budgets streamlined and focused on the most prolific shale plays, U.S. drillers are giving OPEC a hard time by raising output and hedging future production. Meanwhile, the cartel members are trying to cut supply and fix the price of oil at such a range that would allow them to reap higher oil revenues, but not allow the shale patch to recover too much too fast.

Two and a half months into the supply-cut deal, it looks like OPEC is losing the campaign to prop up oil prices. The drop in prices that began last week saw them retreating to almost exactly the same level as on November 30 – just below $52/barrel for Brent – when the OPEC deal was announced, the International Energy Agency said in its monthly report on Wednesday.

At the same time, reduced breakeven prices in many shale plays and forward locking-in of production is allowing the companies currently drilling in the U.S. to turn in profits even at a price of oil at $40 a barrel. The U.S. shale patch has not only emerged leaner and more resilient from the downturn, it has also hedged future production with contracts guaranteeing the price of the crude they will be pumping a year or two from now, Bloomberg reports, citing industry executives and analysts.

This is a sign that OPEC may have underestimated—yet again—the resilience of the U.S. shale patch when the cartel decided to collectively curtail oil supply.

Last week Saudi officials told American oil producers that there would be “no free rides” and that they should not expect OPEC to extend or deepen the output cuts to make up for the jump in shale production in the U.S.

And U.S. shale output has been steadily growing in the past few months, thanks to, and quite ironically so, OPEC’s cuts that have been supporting WTI prices at above $50 (or at least above $48 this past week). The U.S. shale patch is expected to lift its April oil output by 109,000 bpd, the EIA said earlier this week.