There are two questions here of course:

- How will oil price develop over the next 2 years? And the only certain thing is that forecasts will be wrong, and

- Can the net difference between the positive effect on oil consuming countries and the negative effects on oil producing countries be sufficient to lift the global ecoonmy out of its doldrums?

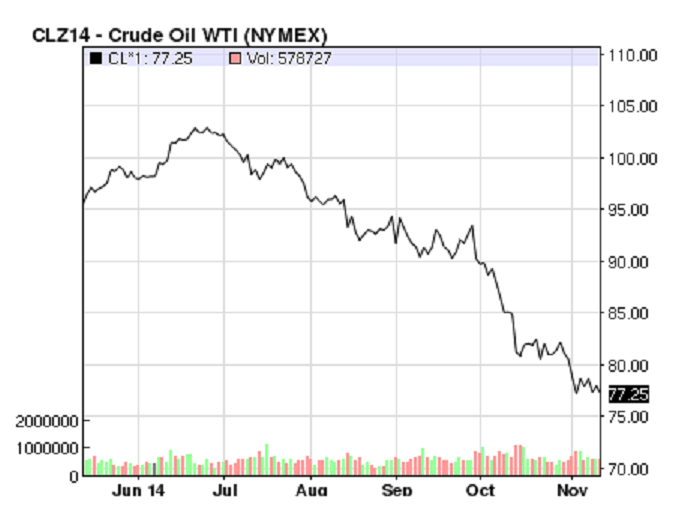

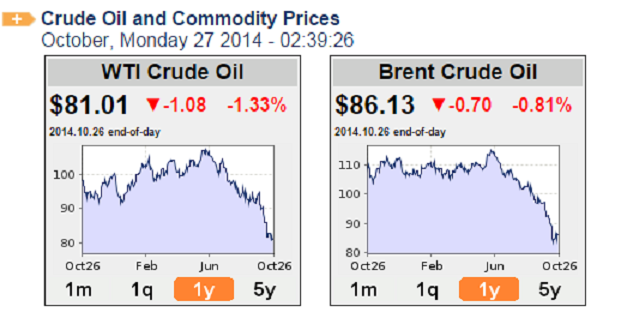

Oil prices have dropped 25% since June and currently WTI crude is at $81 and Brent crude is at $86 – down from around $110 – 115 in June. How far can prices drop and for how long? Of course this depends on supply and demand. But I think there is a new paradigm here and created by the injection of shale oil into the mix. I suspect that shale oil production now establishes a new floor price which means that the prices cannot drop lower than about $60 or possibly even $70. Oil from the traditional, large oil wells can still be produced profitably at much lower prices. But shale oil is more expensive to produce partly due to the costs of fracking but also due to smaller individual wells which last for shorter periods than the large oil wells. This in turn means that there is both a higher investment cost and a higher operating cost for shale oil compared to “traditional” oil. It is thought that as shale oil increases its contribution to the total mix, this production cost will set a floor for all oil at around $60-70 instead of the $30-40 needed for break-even (zero exploration) with traditional oil. The oil companies will maintain profits and dividends by scaling down jobs and their new exploration costs which is the variable they can play with . It is the oil producing countries who will lose tax revenues (offset by increased production – if any).

oil price 27102014 oil-price.net

Goldman Sachs have forecast in a new research report that prices could drop to $70 by the second quarter of 2015.

Reuters 27/10: Brent crude futures fell below $86 a barrel on Monday after Goldman Sachs cut its price forecasts for the contract and for U.S. oil in the first quarter of next year by $15.

The U.S. investment bank said in a research note on Sunday that it had cut its forecast for West Texas Intermediate to $75 a barrel from $90 and that for Brent to $85 from $100, with rising production in non-OPEC countries outside North America expected to outstrip demand.

The bank expects WTI to fall as low as $70 a barrel and Brent to hit $80 in the second quarter of 2015, when it expects oversupply to be most pronounced.

Even Saudi Arabia now seems to have accepted that a regime of low prices will last 1 – 2 years.

Reuters 26/10: The recent decline in global oil prices will prove temporary even if it lasts a year or so, since population growth will ultimately bring higher consumption and prices, the chief executive of Saudi Basic Industries Corp said on Sunday.

Mohamed al-Mady was speaking to reporters after the company, one of the world’s largest petrochemicals groups and the Gulf’s largest listed company, reported a 4.5 percent drop in third-quarter net income, missing analysts’ forecasts.

At these price levels for 2 years almost $3 trillion will shift from the “few” producers to the “many” consumers. But most of this could fuel consumer growth (which it would not do to the same extent when in the hands of the oil producers). The consumer countries will also lose the foreign exchange constraints they must operate under for purchase of oil in US Dollars. It could release monies desperately needed for infrastructure projects. But the consumer countries need the prices to stay low for some time – and I would guess that 2 years is a minimum – for the public funds released to be utilised in “growth” projects.

The Economist: For governments in consuming countries the price fall offers some budgetary breathing-room. Fuel subsidies hog scandalous amounts of money in many developing countries—20% of public spending in Indonesia and 14% in India (including fertiliser and food). Lower prices give governments the opportunity to spend the money more productively or return it to the taxpayers. This week India led the way by announcing an end to diesel subsidies. Others should follow Narendra Modi’s lead.

Producer countries will be hit. Russia has actually been helped by the fall in the rouble which has cushioned – a little – the rouble values of the dropping oil revenue.

The most vulnerable are Venezuela, Iran and Russia.

The first to crack could be Venezuela, home to the anti-American “Bolivarian revolution”, which the late Hugo Chávez tried to export around his region. Venezuela’s budget is based on oil at $120 a barrel. Even before the price fall it was struggling to pay its debts. Foreign-exchange reserves are dwindling, inflation is rampant and Venezuelans are enduring shortages of everyday goods such as flour and toilet paper.

Iran is also in a tricky position. It needs oil at about $140 a barrel to balance a profligate budget padded with the extravagant spending schemes of its former president, Mahmoud Ahmedinejad. Sanctions designed to curb its nuclear programme make it especially vulnerable. Some claim that Sunni Saudi Arabia is conspiring with America to use the oil price to put pressure on its Shia rival. Whatever the motivation, the falling price is certainly having that effect.

Compared with these two, Russia can bide its time. A falling currency means that the rouble value of oil sales has dropped less than its dollar value, cushioning tax revenues and limiting the budget deficit.

There are a number of other effects of $70 per barrel for oil.

Bio-fuels and bio-diesel, which are fundamentally unsound, have stayed alive on the back of subsidies on the one hand and a high oil price on the other. If the prices stay at $70 for 2 years or longer, land currently being wasted on bio-fuels could revert to food production. With lower fertiliser and transport costs in addition, a great deal of pressure on food prices go away. If the floor price is set by shale oil production costs, it may be too low for oil production from tar sands to take off in any big way. Electricity production costs will be bench-marked against the cost of gas turbine combined cycle plants.

But most importantly, another 2 years or longer with the public spending pressures reduced will allow a number of other countries to get their own shale oil (and gas) production going. And that will make Opec and the oil cartel obsolete. Oil and gas price speculation will no longer be possible.

It could provide the start for a long sustained period – perhaps even a decade or two – with oil prices stable at around $70 per barrel.