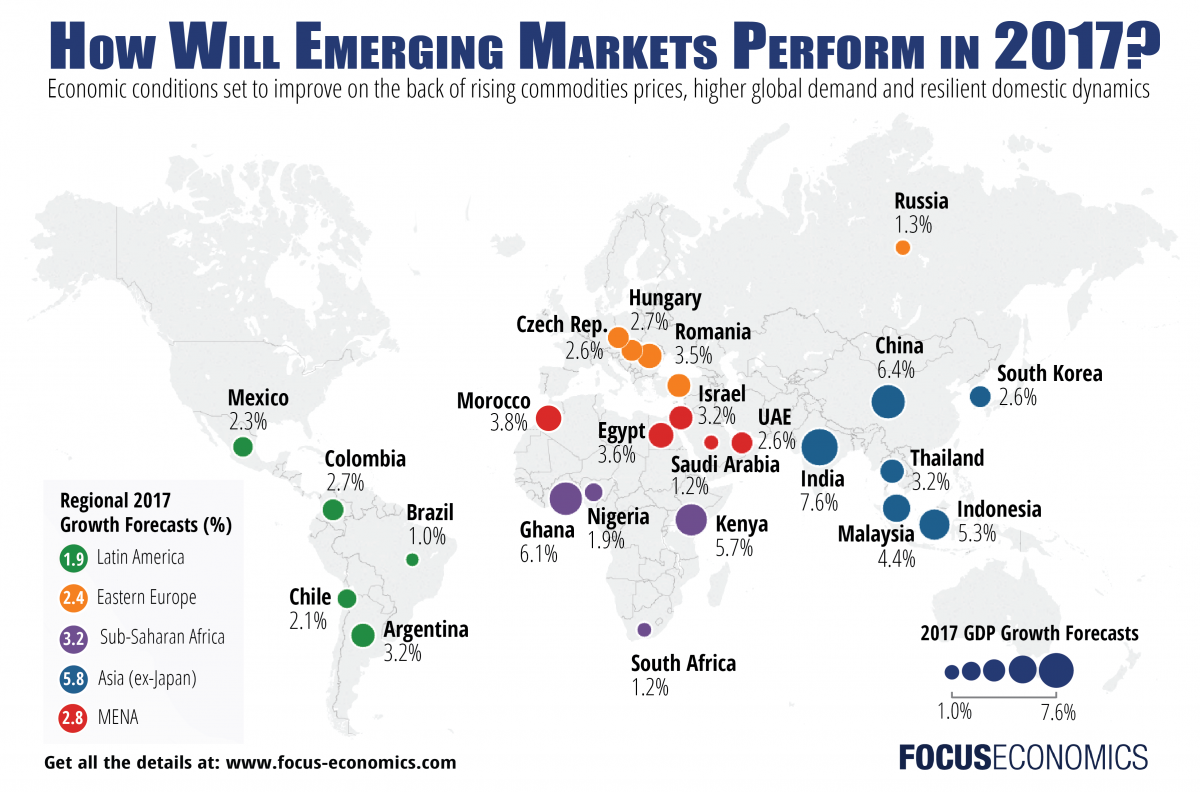

Focus Economics has published its emerging markets prediction for 2017.

- Latin America | External shocks to undermine potential growth in the region

- Asia | Growth will benefit from rising global demand and resilient domestic dynamics

- MENA | Higher oil prices promise to boost growth in 2017

- Eastern Europe | Economic conditions set to improve in 2017

- Sub-Saharan Africa | Weak growth urges policy action

Focus Economics: Emerging Markets outlook 2017

It is in Asia and a recovering Russia that there may be some drive:

Asia | Growth will benefit from rising global demand and resilient domestic dynamics

- China’s still resilient economic growth and the ongoing reform momentum in India will prompt the East and South Asia (ESA) region to expand a strong 6.0% in 2017, which will represent a slight deceleration from the expected 6.1% increase in 2016. Meanwhile, in the Association of Southeast Asian Nations (ASEAN), an improvement in the region’s external sector should support quicker growth along with resilient household spending. ASEAN will expand 4.8% in 2017, up from 2016’s 4.6% increase.

- Inflationary pressures are expected to strengthen across Asia next year as a result of a low base effect, the gradual increase in commodity prices and scheduled subsidy cuts and tax hikes in some economies. While inflation in ESA will increase mildly from 2.4% in 2016 to 2.5% next year, the pick-up in ASEAN will be more pronounced and inflation is expected to rise from 2.3% in 2016 to 3.2% in 2017.

- While economic growth in the region will benefit from a mild improvement in global demand and resilient domestic dynamics, some clouds are gathering on the horizon. Donald Trump’s victory in the U.S. presidential elections could disrupt the global economy if he implements his proposed protectionist policies. This has the potential to hit growth in the region, given the importance of the external sector for most Asian economies. Also, a more aggressive monetary policy normalization by the U.S. Federal Reserve could heighten volatility in the financial and exchange rate markets in the region.

………

Eastern Europe | Economic conditions set to improve in 2017

- The stabilization of commodities prices and the economic recovery in Russia, the region’s largest economy, should support a return to growth in the Commonwealth of Independent States (CIS) region next year. GDP is seen growing 1.5%, after falling 0.3% in 2016. However, geopolitical risks and monetary tightening in the U.S. are casting a shadow on the outlook.

- In Central & Eastern Europe (CEE), steady domestic demand should fuel a healthy 3.0% growth this year and next. Meanwhile, dynamics in South-Eastern Europe (SEE) will be dominated by escalating political uncertainty and security concerns in Turkey and the ongoing debt saga in Greece. GDP in SEE is seen expanding 2.8% in 2017, slightly above the 2.7% projected for this year.

- Price pressures in the CIS region should fall steadily throughout 2017, supported by a tightening bias by most central banks in the region, and our panel sees inflation at 5.6% in 2017. For CEE, inflation is expected to rise in 2017 as the effect of low oil prices wanes, with our analysts projecting average inflation of 1.5%. Meanwhile, SEE will see a slight increase in price pressures on the back of rising inflation in Greece and Romania.

- External risks to the Eastern European economy are high heading into 2017. The surprise outcome of the U.S. presidential election along with tense Brexit negotiations will increase volatility in the financial markets and weigh on currencies and assets across the region. In addition, an expected increase in U.S. interest rates has the potential to tighten global liquidity and spark capital outflows. For Russia, however, Trump’s election is seen as positive and some analysts speculate that he could end sanctions against Russia due to his close ties with the country.

Maybe the financial crisis which started in 2008 is finally coming to an end. Eight years is long enough.

I blame the EU and the lack of drive from Barack Obama, not for the start of the crisis, but for prolonging the length of time it has lasted. But one reaction for the political cowardice of the last 8 years (some would say 20 years) is the disenchantment with liberal/social democratic, politically correct, elite and “establishment” politics.

The disenchantment is showing itself to be a global phenomenon.