Obamacare costs are no longer affordable. So even Barack Obama is comparing his Affordable Care Act with Samsung’s Galaxy Note 7.

“When one of these companies comes out with a new smartphone… [and] it has a few bugs, what do they do, — they fix it, [they] upgrade it. Unless it catches fire – then they pull it off the market”.

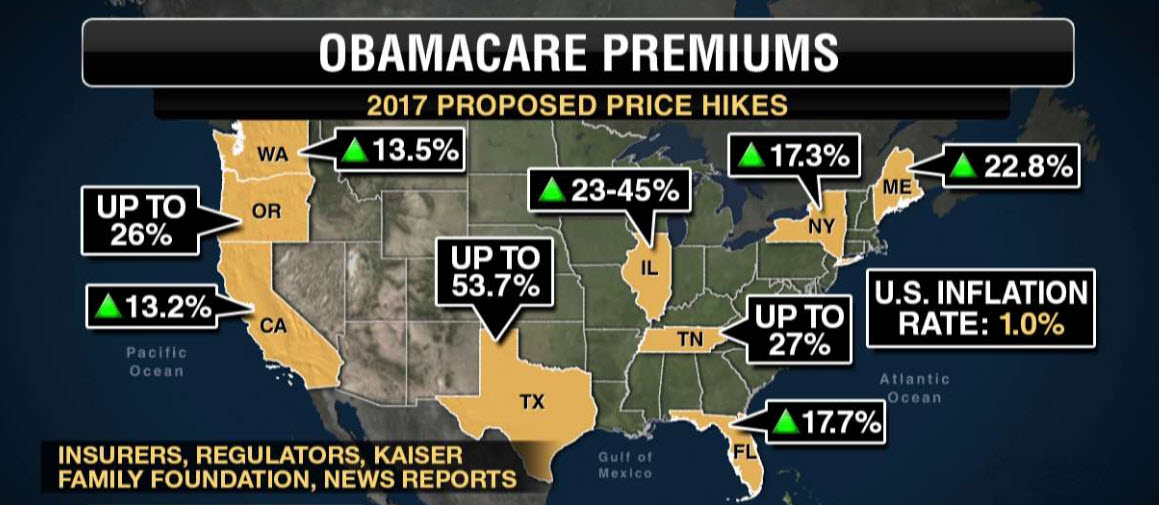

And Obamacare is clearly on fire.

obamacare-premiums-2017-graphic-zerohedge

Obamacare’s Collapsing. That Was Always The Plan.

On Thursday, President Obama attempted to defend the skyrocketing costs of Obamacare by comparing them to the Samsung Galaxy Note 7, a smartphone that was banned on airplanes because it had a nasty habit of spontaneously combusting. …. Obama put the responsibility on the states for not expanding Medicaid, thereby avoiding picking up the costs of Obamacare. The vast majority of people who have enrolled in Obamacare have done so at point of government gun, and have done so as part of the Medicaid expansions Obamacare attempted to incentivize; as of October 2015, nearly all of the “newly insured” enrollees were Medicaid enrollees. Obama tried to claim that the federal government would pick up the tab for expanded Medicaid, but that neglects that over time, the states pick up more and more of the tab – and that the federal government is $20 trillion in debt.

Now, Obama’s pushing the public option, using George W. Bush’s egregiously awful Medicare Part D prescription drug benefit expansion. Part D has led to massive increases in healthcare costs, as well as to rejection of Medicare itself by health providers thanks to government restrictions on costs. As Mark Levin writes in Plunder and Deceit, “the impracticability of Medicare’s centralized management and archaic decision-making practices…significantly impairs the broader private sector.” …

….. I told Fox News back in August 2013 that Obamacare was designed to fail, thereby necessitating a government option. That option would bankrupt insurance companies – the government doesn’t have a necessity for profit margin, and therefore, for decent service – and lead to the complete government takeover of healthcare Obama has always sought. In other words, Obamacare was created with designed obsolescence – it’s as though Samsung had designed their phones to melt down so that they could then market the Samsung Galaxy Note 8, Government Edition.

Obamacare is not the shining example some people would like to pretend it is.