Oil prices have “crashed”.

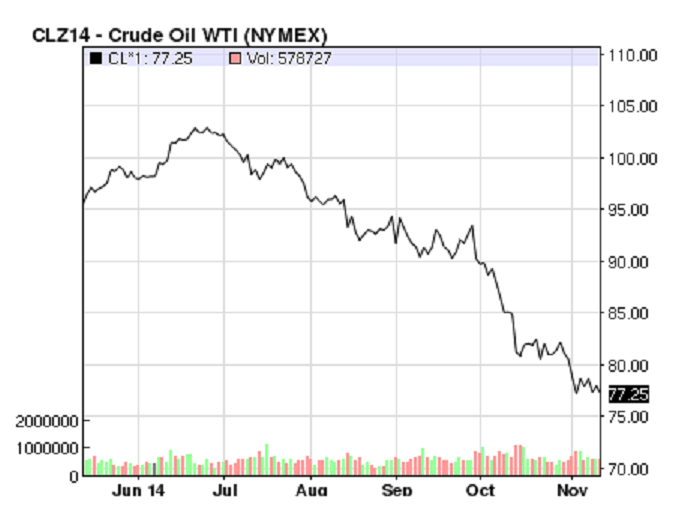

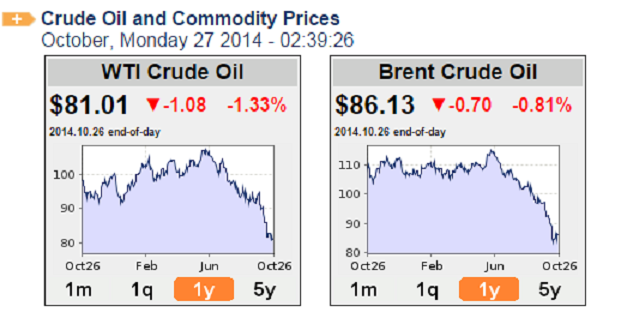

Currently prices are at less than $80 per barrel compared to over $110 in June and the peak of $147 just before the financial bubble burst in 2008. It seems that it is due to the oil glut brought about by the shale oil revolution in the US together with a downturn in global growth. The $147 peak was, I think, more of a trial balloon by the oil producers to test where the resistance lay and the producers concluded that a level of a little over $100 would maximise profits and was sustainable. But I suspect that this $100 level itself has contributed to delaying and prolonging the recovery. Not only because of the increased direct costs to the oil consumer but also due to its knock-on effects which have unnecessarily raised the cost to all electricity consumers. The prolongation of the path to recovery in Europe is certainly – if only partly – due to the very high energy prices that prevail. But right now it is the abundance of shale oil and gas which seems dominant.

Bloomberg: But the bigger factor appears to be surging global oil production, which outpaced demand last year and is shaping up to do so again in 2014. To try to keep prices high, Saudi Arabia, the world’s biggest petroleum exporter, has reduced its oil production from 10 million barrels a day—a record high—in September 2013 to 9.6 million as of Sept. 30. That hasn’t done much to raise prices, mostly because other OPEC countries are pumping more crude as the Saudis try to slow down. Sharply higher production increases from Libya and Angola, along with surprisingly steady flows out of war-torn Iraq, have pushed OPEC’s total output to almost 31 million barrels a day, its highest level this year and 352,000 barrels a day higher than last September. Combined with the continued increase in U.S. oil production, the world has more than enough oil to satisfy current demand.

crude oil price history 2000-2014

But this crash in oil prices is probably a “good thing”.

The additional revenues from increasing oil price to the few in the oil producing countries have not been sufficient to counter the hit to the many in the consuming countries. Much of the additional revenue has gone not to fuelling growth but in blowing up new real-estate bubbles.

The additional spending power in consumer countries with reducing oil price is spread among the many (at the lower end of the wealth scale) whereas the reduction in producer oil revenues is generally spread among an affluent few. My contention is that the additional revenues with high oil price in – for example – the Middle East does not need to be spent on real things which could fuel growth. Revenues in Saudi Arabia and Qatar and other countries have fuelled bubbles and jihad instead of just growth. A great deal went instead into very high margin, weapons systems and to the imaginary values of real estate. In Russia the oil revenue did contribute to some growth but there was still a large proportion spent on imaginary values of various bubbles (which by definition cannot contribute to growth). My simple calculation tells me that 1000 people buying washing machines in China contribute more to global growth than one person spending the same amount on an apartment (his second or third home) in London. A $10 drop in oil price is said to shift 0.5% GDP growth from producer countries to consumer countries. But the pattern of consumption where the “few” fuel the bubbles of imaginary value while the “many” consume mundane goods and services means that the real effect on growth is greater than a net zero. It is shifting an ineffective 0.5% to a more efficient consumption for growth. The net effect is probably a growth in global GDP of 0.2 – 0.3%. Similarly the purchase of large-volume, low-margin goods and services provides more growth and jobs than spending the same amount on low-volume, high margin goods and services. Spending $1000 on an 80% margin Gucci handbag provides less direct growth and fewer direct jobs than buying ten $100, 10% margin travel bags.

Historically – though it is a relatively crude generalisation – low oil price has usually given – or coincided with – consumer-led growth and stability.

crude oil price history 1970-2014

Some oil producers are more vulnerable than others to the fall in expected revenues. Russia’s budget needs an oil price of over $100 to be balanced. Venezuela spends nearly all of its revenues as it is generated and has nothing put by. The war-torn areas of the Middle East also have nothing put by. Saudi Arabia and the Gulf States have put by vast reserves though some of it is in “bubble” values. A pricking of some of the bubbles they have inflated is probably no bad thing. It is also no bad thing if they have to fall back on reserves and have less excess cash to fund jihadists from Afghanistan to Libya.

Most Asian countries are oil importers and gain from a low oil price.

Clarion Ledger: The picture is reversed in Asia, where most countries are major importers and some subsidize the price of fuels.

China is the second-largest oil consumer and on track to become the largest net importer of oil. Falling prices will provide China’s economy some relief, according to Huang Bingjie, professor from the School of Economics and Management at China University of Petroleum. But lower oil prices won’t fully offset the far wider effects of a slowing economy.

India imports three-quarters of its oil and analysts say falling oil prices will ease the country’s chronic current account deficit. Samiran Chakraborty, head of research in India for Standard Chartered Bank, also says the cost of India’s fuel subsidies would fall by $2.5 billion during its current fiscal year if oil prices stay low.

Japan imports nearly all of the oil it uses. Following the accident at the Fukushima Dai-Ichi nuclear power plant in 2011, Japan has turned more to oil and natural gas, which is priced based on oil, to generate electric power.

The picture is a little more mixed in the Americas and Europe:

Low prices could eventually threaten the boom in oil production in such countries as the U.S., Canada, and Brazil because that oil is expensive to produce. Investors have dumped shares of energy companies in recent weeks, helping to drag global stock markets lower.

For now, lower crude oil and fuel prices are a boon for consumers. In the U.S., still the world’s biggest oil user, consumer spending accounts for two-thirds of the U.S. economy, and lower energy prices give consumers more money to spend on things other than fuel.

The same is true in Europe. Christian Schulz, senior economist at Berenberg Bank, says that a 10 percent fall in oil prices would lead to a 0.1 percent increase in economic output. That’s meaningful because the 18-country currency union didn’t grow at all in the second quarter.

There could be another market crash coming though it is not likely to be as deep as the 2008 crash. But to get back onto a solid, sustainable growth path again it does need the oil consumer countries to grow. And that probably needs a steady oil price at less than $70 per barrel. The oil producer countries will have to revamp their economies to live with the loss of their monopoly as the production of oil from shale spreads.