Being poor is a relative term. To be in “extreme poverty” is an absolute measure. To be “poor” does not require being in “poverty”. The “poor” relative to the “rich” will always be with us and are just as necessary as the “rich”. In fact, that distinction between rich and poor is necessary as long as humans are to be considered individuals with aspirations and not just clones. Income inequality is often equated – especially by those with communistic leanings – with poverty, but this is simply wrong. Income inequality may be an indicator of the ratio of “poor” to “rich” but to be “poor” need have nothing to do with being in “poverty”. “Poverty” is not necessary and the goal is to eliminate extreme poverty by 2030.

The 2015 World Bank Research Note on Extreme Poverty is now out. In 2015, for the first time ever, and in spite of the global population being at an all time high, the number of people in extreme poverty has reduced to less than 10%. In spite of the population increase, the total number in extreme poverty is at the lowest in 25 years. But that is still 700 million (900 million in 2012) in extreme poverty. Sub-Saharan Africa and S Asia are where the misery is concentrated.

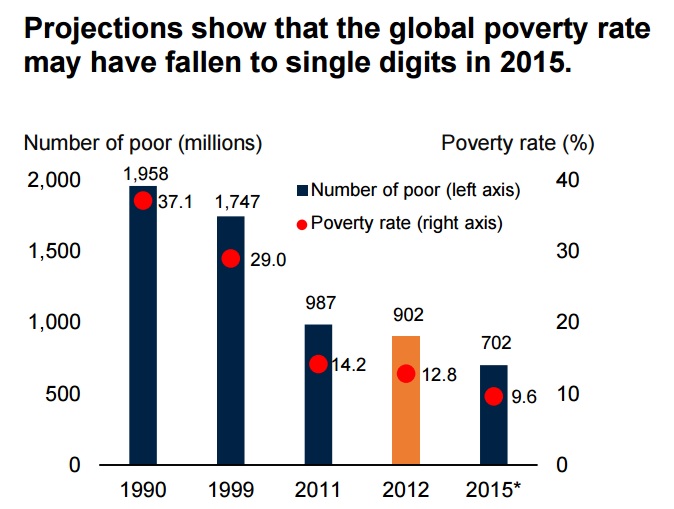

Extreme Poverty – World Bank 2015

The number of people living in extreme poverty around the world is likely to fall to under 10 percent of the global population in 2015, according to World Bank projections released today, giving fresh evidence that a quarter-century-long sustained reduction in poverty is moving the world closer to the historic goal of ending poverty by 2030.

The Bank uses an updated international poverty line of US $1.90 a day, which incorporates new information on differences in the cost of living across countries (the PPP exchange rates). The new line preserves the real purchasing power of the previous line (of $1.25 a day in 2005 prices) in the world’s poorest countries. Using this new line (as well as new country-level data on living standards), the World Bank projects that global poverty will have fallen from 902 million people or 12.8 per cent of the global population in 2012 to 702 million people, or 9.6 per cent of the global population, this year.

Extreme Poverty contributions – World Bank 2015