Shale oil production in the US seems to have resisted the Saudi attack. While some of the smaller wells have decreased and even stopped production, they can restart very quickly if and when the price is right. US inventories are extremely high, but perhaps of more significance in the long run is that with the pressure of low oil price, shale oil production costs have come down drastically. The Saudi attack on shale has only forced cost cutting measures which the shale industry had not bothered with when prices were high.

Wells which were thought to have a break-even oil price of $60/brl have come down to $40 and those thought to have been at $40 are now closer to $20. Of course they are a long way from Saudi production levels of about $3/brl, but it is the Saudi attack which has now improved their competitive position. Europe – when it eventually gets past its debilitating green lobbies – will be able to take advantage of the much improved and streamlined shale oil production process. Shale oil with a production cost around half of that from the North Sea could provide a bigger boost for the England economy than North Sea gas provided for Scotland.

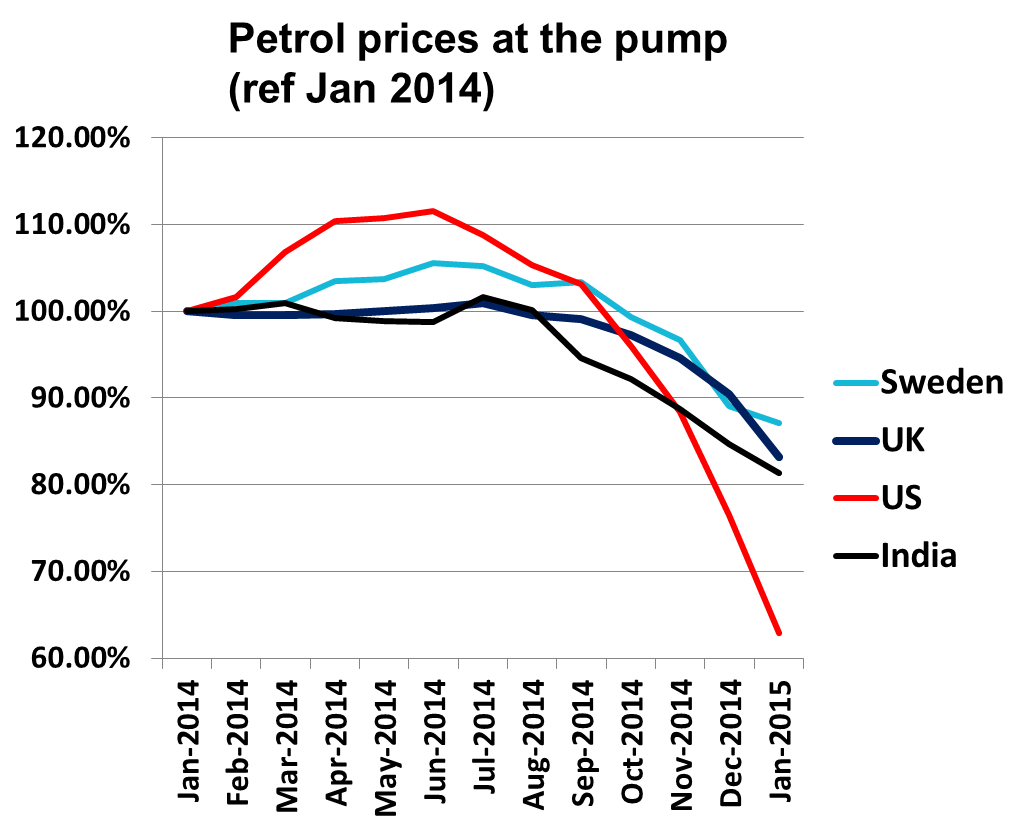

Saudi shale war

It is still a bit of a mystery as to why oil price has stabilised above $50 when inventories are so high. It is probably because OPEC was expecting to take greater market share – which they haven’t – in a recovering Chinese economy – which has not yet happened. The pressure on price is downwards and the current stability is probably temporary. It is likely that oil price is in for almost 2 years at a price averaging around $45/barrel or less.

US oil inventories may 2015 (EIA)

Reuters: The North American oil boom is proving resilient despite low oil prices, producer group OPEC said in its biggest and most detailed report this year, suggesting the global oil glut could persist for another two years. A draft report of OPEC’s long-term strategy, seen by Reuters ahead of the cartel’s policy meeting in Vienna next week, forecast crude supply from rival non-OPEC producers would grow at least until 2017.

Sluggish global demand for oil means the call on OPEC’s crude will fall from 30 million barrels per day (bpd) in 2014 to 28.2 million in 2017, effectively leaving the group with two options – cut output from current levels of 31 million bpd or be prepared to tolerate depressed oil prices for much longer.

….. Brent crude has collapsed from $115 a barrel in June 2014 due to ample supplies amid a U.S. shale oil boom and a decision by OPEC last November not to cut output. Instead the group chose to increase supply in a bid to win back market share and slow higher-cost competing producers.

But shale oil production has proved to be more resilient than many had originally thought. “Generally speaking, for non-OPEC fields already in production, even a severe low price environment will not result in production cuts, since high-cost producers will always seek to cover a part of their operating costs,” the OPEC report said.

…… since 1990, most of the forecasts concerning future non-OPEC oil supply have been pessimistic and often erroneous: “For example, non-OPEC production was once projected to peak in the early 1990s and decline thereafter.”