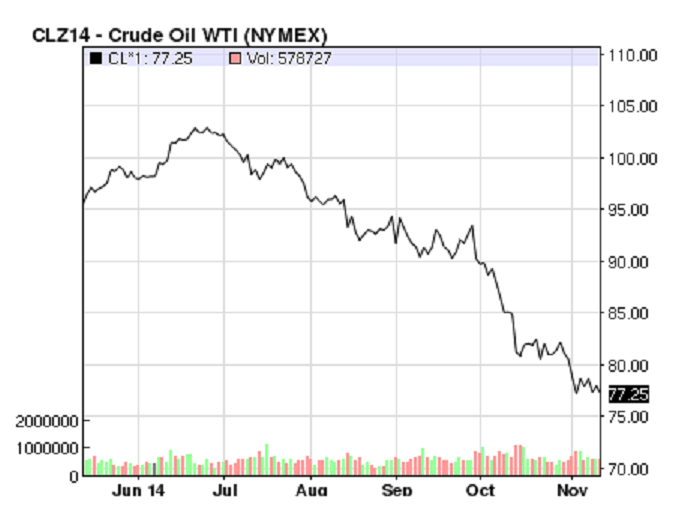

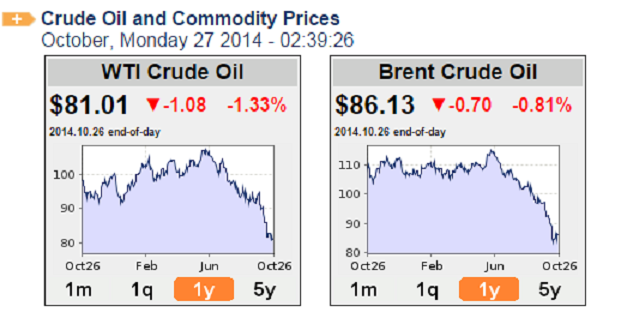

Currently US crude is at just above $76 per barrel and Brent oil is at about $80. OPEC members are meeting this week in Vienna and it is thought that cuts to oil production of between 0.5 million and 1.5 million barrels per day (bpd) are possible. The drop in oil prices since June (from around $110 per barrel is due to a glut which in turn is due to over production, large quantities of US shale oil becoming available and simultaneously a reduced demand from China and others. Saudi Arabia is conspicuous by not having made any significant production cuts so far. This could be due to one of 3 reasons:

- Saudi Arabia is testing the breaking point for some of the shale oil producers since some of the smaller shale wells probably have a break-even level of around $60-70 per barrel, or

- Saudi Arabia and the US are targeting Russia and Iran whose economies are vulnerable and very dependent on the oil price (and the Russians alone would lose some $100 billion in oil revenues per year), or

- Saudi Arabia is tired of bearing the brunt of the production cuts and is forcing some of the smaller OPEC producers to take their share of the pain of production cuts.

If cuts of less than 0.5 million barrels per day are made it is thought that the prices are headed down to about $60 per barrel. One analyst estimates that a cut of 2 million bpd is needed to get back up to $80 per barrel. Something in between will be – well – something in between.

I just don’t like cartels and especially when they are state sponsored cartels. So far shale oil production is just from the US, and the OPEC strangle-hold on oil price has yet to be broken. But, over time, I expect this cartel to weaken as other countries produce oil and gas from shale. I remain of the opinion that the OPEC cartel has – no doubt – enriched the oil producing countries but has only done so at the expense of the rate of development of non-producers. OPEC has done the global economy a disservice by holding back the developing countries and the strongest correlation in geopolitics is the link between energy consumption and development (not just GDP but also virtually every development parameter).

It may cause some short term turbulence but in the long run it will be a “good thing” even if oil price were to collapse to below $50 per barrel. Some producers will be hard hit but the net result for the global economy will be positive. So I shall be quite happy if OPEC cannot reach agreement on how much oil production to cut or if they make just a small cut. It is time for some of the the developing countries to get a break from the oil price extortion which has been in place since 1973. The sooner the OPEC cartel is rendered obsolete the better.

Some commodity fund managers believe oil prices could slide to $60 per barrel if OPEC does not agree a significant output cut when it meets in Vienna this week. Brent crude futures have fallen by a third since June, touching a four-year low of $76.76 a barrel on Nov. 14. They could tumble further if OPEC does not agree to cut at least one million barrels per day (bpd), according to some commodity fund managers’ forecasts. …..

Yet fund managers and brokerage analysts are divided over whether OPEC will reach an agreement on cutting output. Bathe put the likelihood at no more than 50 percent. Oil prices have been falling since the summer due to abundant supply, partly from U.S. shale oil, and because of low demand growth, particularly in Europe and Asia. As a result, some investors believe a small cut of around 500,000 bpd would not be enough to calm the markets. Doug King, chief investment officer of RCMA Capital, sees Brent falling to $70 per barrel even with a cut of one million bpd.

“With this, I would expect lower prices in the first half of 2015,” he said. If OPEC fails to agree a cut, prices will drop “further and quite quickly”, with U.S. crude possibly sliding to $60, he said. U.S. crude closed at $76.51 on Friday, with Brent just above $80. ……..

The market has been awash with conspiracy theories as to why Saudi Arabia has not already intervened. New York Times columnist Thomas Friedman hinted at “a global oil war under way pitting the United States and Saudi Arabia on one side against Russia and Iran on the other”. Hepworth argued that Saudi Arabia appeared pretty happy with current pricing levels and suggested they were waiting to see where the cut-off point for U.S. production was. “Time is on their side, they can afford to wait,” he said, stressing he was talking months, not years, but added if oil fell below $70 that waiting time “shrinks to weeks”.

Tom Nelson, of Investec Global Energy Fund, said he believed Saudi Arabia had allowed the price to fall to incentivise smaller OPEC producers, which often rely on the biggest producer to intervene, to join Riyadh in cutting output. “They (the Saudis) want to cut but they don’t want to cut alone,” Nelson said, adding that a cut of between one million and 1.5 million bpd should be sufficient to balance the market.

“The market really wants to see that OPEC is still functioning … if there is a small cut, with an accompanying statement of coherence from OPEC that presents a united front, and talks about seeing demand recovery, and some moderation of supply growth, then Brent could move up to $80-$90.”